My wife and I are long-term investors. Before deciding to invest in a stock or fund we do a lot of research to estimate its long-term potential. If that investment performs well we hold onto it, waiting until we have available cash from the next year's savings to pick a new investment.

We have been married for almost seventeen years. Most years we did what economists recommend and saved at least ten percent of our earnings.

(There were a couple years where home improvements meant we saved less, but often our house value went up. During the two years when each of our boys were born we spent a bit more than we earned due to my wife being on maternity leave.)

Einstein may have once called compound interest either "greatest invention in human history" or "the most powerful force in the universe". In any case, it should not be surprising that after seventeen years our investments had appreciated greatly.

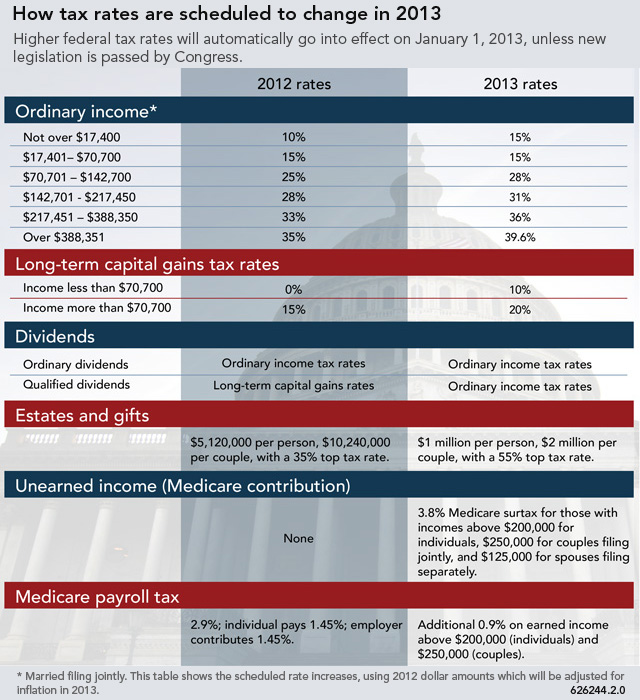

December ended with a potential fiscal cliff and doubts about whether 2012 would be the last time to long-term capital gains without taxes if your total taxable income was less than seventy thousand dollars.

I have written before about our income: our taxable income is typically a lot less that that cutoff. However, that seventeen years of capital gains would more than double our normal income. So we decided to sell all of our investments with long-term gains, but first needed to donate a big portion of our appreciated investments to charity to stay under that cutoff to avoid paying tax on our long-term gains.

We were happy to find out about Fidelity Charitable. It is charity that holds onto the money you donate, and whenever you give an order it sends out a check to other charities. To paraphrase, it is a tax trick: my family effectively paid several years tithes "up front" for a tax benefit in 2012, and for a while will pay our tithes from our Fidelity Charity account instead of our bank account.

My wife and I are very used to a mindset in which we do not consider our investments "our money". First, because we see ourselves as stewarding a portion of God's money that in the long term is not ours. Second, because our investments have always been "sticky" instead of liquid since we could not easily sell them without worrying about tax implications.

Now it seems strange. We have reinvested, and our investments are so much more liquid. It is still God's money, but it is nearer.

There is a nice benefit. Because our investments are now liquid, the money we keep as cash at the credit union for emergencies can be very easily replaced. That means we can more readily offer our close friends interest-free loans.

{kind=link}

No comments:

Post a Comment