Time for a longer essay about the Stimulus Plan, focusing on the two big questions.

1. What type of government plan would best stimulate the economy?

2. How soon would a recovery happen?

Since I am a mathematician, not an economist, I cannot answer these questions with any confidence. But then, neither can the economists. All I can do is read what brilliant economists have written and apply it to today, fourteen months into the current recession. This essay will discuss the implications of two essays by Milton Friedman.

Friedman's first article is straightforward and easy to read. He discusses the options for how the government could get the money for a stimulus plan (taxes, debt, printing more money) and their effects.

Friedman concludes that the most reliable plan for stimulus would be to print money and use it to buy existing government bonds. Historically a one-time printing of money need not lead to inflation, and removing government bonds from the market would move money previously used in those investments to private consumption or investment.

Oddly, few politicians or reporters are considering the long-term effects of paying for the current Stimulus Plan. Most are doing the opposite and accepting without proof that a short term plan of debt to fund work will have a longer term affect of overall creating jobs.

Friedman's second article is a classic analysis of how recessions end. Its comparison of three historical recessions deserves a bit more commentary.

Remember my post sharing how my family's investments are down to what they were three years ago? That fits nicely with his third chart: the market is about where it was three years previously one year into all of those three historical recessions. But the three recessions diverge wildly soon after. Which will this recession most resemble?

The main claim of the second article is that a faster growth of M2 corresponds with a prompter recovery (Friedman's figure 1). During the past few years M2 has been growing rapidly. This is very promising.

Also, although GDP fell during the last half of 2008 it decreased less than 5% total, which is not alarming (figure 2). The M2 affect should dominate, so the current recession will probably be more mild than those other three. However, note that according to Friedman's analysis even "more mild" means continued market loss for another year or two (figure 3).

In conclusion, Friedman's answer to the two big questions is that the government should print money, use it to buy existing government bonds, and plan on at least another year of market loss.

The economy is in recession but not in shambles. (Rather, it is a sound habit among individuals, corporations, and states of having a cash reserve instead of debt that causes trouble--with some notable exceptions.) There is no need for so much alarm.

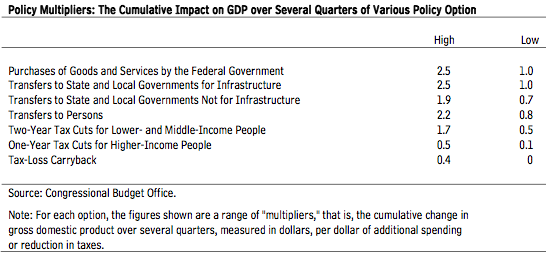

(As a concluding tangent I should also note that there are problems with the proposed Stimulus Plan both legal and economic in nature. It is currently a gamble (article, chart) and thus an easy plan to oppose, but may be improved in future drafts.)

UPDATE: The final sentence has been revised for clarity; it now has a link to the source CBO document and summary table of possible multipliers.

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment